Navigating the July 2026 VAT Change: A Guide for Hospitality & Hairdressers

For some companies in the hospitality sector, as well as hairdressers, the rate of VAT is reducing from 1 July 2026. The aim of the VAT reductions is to support the hospitality sector as companies struggle with higher costs, including higher food and energy costs.

This blog outlines the changes in VAT rates, who they apply to, and the types of products/services they apply to. We’ll also provide some tips and best practices for businesses where VAT rates are changing.

VAT Rate Changes for Hospitality Businesses and Hairdressers Starting 1 July 2026

The new VAT rates, which come into effect from 1 July 2026, apply to:

- Food and drink provided by restaurants, hotels, catering services, and hot takeaways (excluding alcohol, bottled waters, sports drinks, soft drinks, and vegetable juices)

- Hairdressing services.

For products and services that meet the above criteria, VAT will decrease to the second reduced rate of VAT from 1 July 2026. This means a decrease from 13.5% to 9%, representing a one-third reduction in the rate of VAT.

What is Not Included in the July 2026 VAT Reduction

As mentioned above, not all food and drink is included in the VAT reduction. Specifically, there is no change in VAT for sales of alcohol, bottled waters, sports drinks, soft drinks, and vegetable juices, even in restaurants or similar settings.

Also, while the VAT changes apply to food served in hotels, hotel accommodation is not included. In fact, there is no change to the rate of VAT for any type of hotel or guest accommodation.

Apportioning for VAT Purposes

The change in VAT rates has been broadly welcomed by affected businesses, but there are some areas of complexity. This includes situations where businesses will need to apply different VAT rates depending on the services offered.

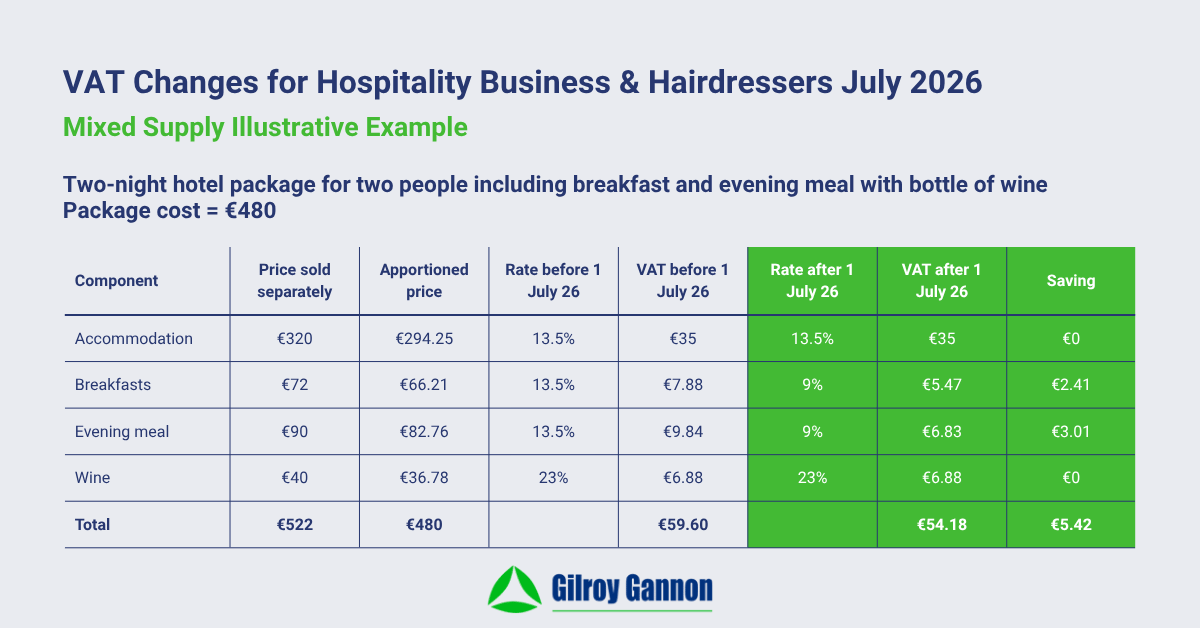

An example will explain how this could apply in practice. The example is a common approach used by hotels in Ireland, whereby package deals are offered to customers at a fixed price. In this example, the package includes two nights’ accommodation, breakfast on both mornings, and one evening meal with a bottle of wine.

In this type of situation, the charge to the customer must be “apportioned for VAT purposes”.

This means splitting all the different elements up so the correct rate of VAT can be applied:

- The second reduced VAT rate of 9% applies to the breakfast and the evening meal, excluding the wine.

- The reduced VAT rate of 13.5% applies to the room for the two-night stay.

- The standard VAT rate of 23% applies to the bottle of wine.

According to guidance from the Revenue, you should split up the costs on a “fair and reasonable basis”, taking into account “the selling prices of each component if sold separately”.

For hairdressers, the above apportioning for VAT purposes can also apply, especially if you sell products like shampoos as well as hairdressing services. Only hairdressing services qualify for the second reduced VAT rate of 9%.

VAT Rates for Restaurant, Catering Services, and Takeaways – Summary Table

Rates applicable from 1 July 2026

| Type of food or drink | Restaurant or catering service | Takeaway |

|---|---|---|

| Alcohol, bottled waters, soft drinks, sports drinks, and vegetable juices | Standard | Standard |

| Cakes, biscuits (other than chocolate-covered biscuits) | Second reduced | Reduced |

| Chocolates, Confectionery, Crisps, Ice cream, Biscuits (chocolate covered) | Second reduced | Standard |

| Coffee, Tea (Hot) | Second reduced | Second reduced |

| Coffee, Tea with confectionery | Second reduced | Second reduced & Standard |

| Coffee, Tea with a scone/ cake | Second reduced | Second reduced |

| Cold Sandwich | Second reduced | Zero |

| Hot Sandwich | Second reduced | Second reduced |

| Fish, Chips, Burgers (Hot) | Second reduced | Second reduced |

| Fish and Chips with a soft drink | Second reduced & Standard | Second reduced & Standard |

| Fruit juices | Second reduced | Standard |

| Take-away Food (Hot) | Second reduced | Second reduced |

| Take-away Food (Cold) | Zero | Zero |

Practical Steps for Your Business

Update Your Systems and Pricing

- Update your accounting software, POS system, and invoicing templates before 1 July. Don’t leave it until the day of the change. Also, test that the correct rates are applying to the correct product/service codes.

- Review your menu or service price list now. Decide whether to pass the savings on to customers to reduce your prices, absorb the savings to improve your margins, or a mix of both. Make the decision and implement it before the rate change date.

- If you use a split-billing or combo deal structure (e.g., meal packages, set menus, event catering, etc), map out exactly which line items attract which rate under the new rules.

Cash Flow and Planning

- The rate change takes effect mid-year, so your VAT returns either side of 1 July will include a mix of the old and new rates. Make sure your bookkeeper or accountant is aware so returns are filed correctly.

- If you’re on cash accounting for VAT, watch out for payments received before 1 July for services delivered after. The rate applicable depends on the tax point, which is typically the invoice date or payment received date, whichever is earlier.

- Model the margin improvement, as a drop in the VAT rate from 13.5% to 9% is meaningful. A good approach is to use the breathing room afforded by the VAT reduction to review your overall pricing strategy rather than passively pocketing the savings.

Mixed-Supply Situations

- If your business offers packages, such as combining accommodation, food, and drink, you need a documented apportionment method in place before July. As mentioned above, the Revenue requires this to be done on a “fair and reasonable basis”. This typically involves referencing the individual selling prices of each component. Best practice is to write this down so it can be referred to and applied consistently.

- Keep records of how you’ve calculated apportionments so you can show your methodology if required.

Staff and Suppliers

- Brief your front-of-house staff on the change, particularly if customers ask questions about pricing or VAT on receipts.

- Check if any of your supplier contracts or service agreements reference VAT rates explicitly, as they might need to be updated.

Don’t Assume Everything Qualifies

- Remember that alcohol, soft drinks, bottled waters, sports drinks, and vegetable juices remain at 23% even when served as part of a meal. If your POS system auto-applies one rate to an entire bill, it will need to be corrected.

- Hairdressers with a product retail element (selling shampoos, styling products, etc.) should note that the rate reduction applies to the service only. Retail product sales have their own VAT rates.

Talk to Your Accountant

- If you haven’t already, now is the time to review your VAT registration status. The rate reduction may affect whether the VAT registration threshold calculation still works in your favour.

- Consider whether the change affects your business plan, financing arrangements, or any forecasts you’ve shared with a bank or investor.

Support from Gilroy Gannon

If you need support ahead of changes in VAT for hospitality and hairdressing businesses, please get in touch with us at Gilroy Gannon.

Latest Blog

Check out our blog and you will get the latest news, events, and financial tips from Gilroy Gannon.

“What's my business actually worth?” This is a question asked…

The fundamentals of statutory audits in Ireland are broadly the…

For some companies in the hospitality sector, as well as…

Agricultural Relief is about facilitating the succession of farm businesses…

Postponed VAT accounting helps Irish businesses improve cash flow by…

Revised Entrepreneur Relief has been around since 2016, but this…

The rate of VAT on the sale of apartments has…

The government’s auto-enrolment pension saving scheme is up and running.…