Entrepreneur Relief 2026: What the €1.5 Million Limit Means for Your Exit Strategy

Revised Entrepreneur Relief has been around since 2016, but this year sees a significant change – the lifetime limit on qualifying gains has been increased from €1 million to €1.5 million.

In this blog, we are going to look at how Revised Entrepreneur Relief works, the impact of the increased lifetime limit, and, most importantly, what it means for your exit strategy.

What is Revised Entrepreneur Relief?

Revised Entrepreneur Relief is a capital gains tax (CGT) relief that reduces the rate of CGT that you have to pay from the standard 33% down to 10%. This means you only pay 10% CGT on qualifying gains up to €1.5 million over your lifetime. For gains made over €1.5 million, the CGT rate is 33%

While the relief doesn’t remove CGT entirely, it can substantially reduce the amount you have to pay. The aim of the policy from the government’s perspective is to encourage entrepreneurs to invest.

Revised Entrepreneur Relief Overview

As mentioned above, Revised Entrepreneur Relief applies to gains made from qualifying assets as follows:

- For self-employed individuals, the qualifying assets must have been owned and used for the purposes of a qualifying business for a continuous period of at least 3 years in the 5 years immediately preceding the disposal.

- In the case of a disposal of shares in a company carrying on a qualifying business, the shares must have been owned by the individual for a continuous period of 3 years at any time prior to the disposal (note the company must have been carrying on a qualifying business during that 3-year period as well.

In terms of the change in the lifetime value from €1 million to €1.5 million, the key date is 1 January 2026. For gains arising before 1 January 2026, you can claim relief on the first €1 million that you make. For gains arising after 1 January 2026, you can claim relief on the first €1.5 million. This means that you can still benefit from the €500,000 increase in the lifetime limit if you have already disposed of assets before 31 December 2025.

What about the “qualifying assets” part of Revised Entrepreneur Relief? The first thing to say is that the criteria are complex. Therefore, to assess your specific circumstances, it is best to review the information on the Revenue’s website and also get expert advice. Our tax advisors at Gilroy Gannon can help.

By way of a brief summary, the main criteria for qualifying assets (in the case of a disposal of shares in a company) include:

- You own at least 5% of the ordinary share capital in the qualifying company (trading company or holding company).

- You must own these shares for a continuous three-year period at any time prior to disposal.

- You must be a director or employee of the company.

- You must have spent at least 50% of your working time in the business.

- You must have held a managerial or technical role.

You must have worked in the company according to the above criteria for a continuous three-year period within the five years immediately prior to disposing of the asset.

It can also be helpful to understand the main types of assets / trades that do not qualify for Revised Entrepreneur Relief. These include development land, investment assets, and assets you own personally outside of the company but which are used by the company for the purposes of its trade.

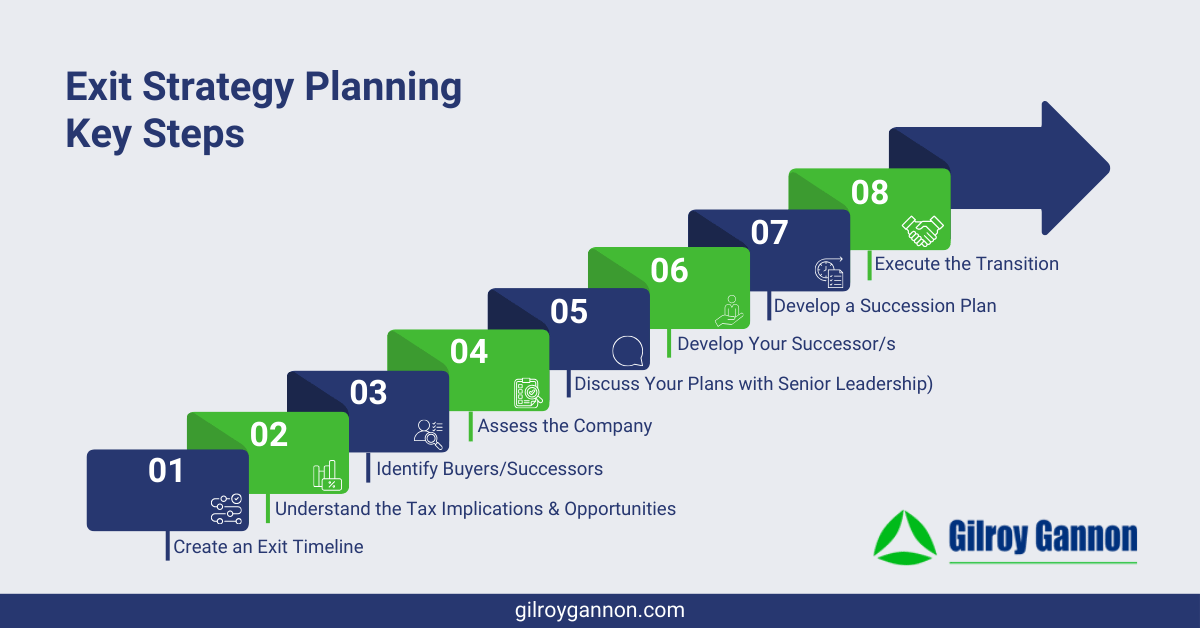

The Impact on Your Exit Strategy

There are many components to an effective exit strategy, including making the transition as smooth as possible, positioning the company for the best chance of future success, and protecting your legacy.

It’s also important to protect the value you have built, including by minimising your tax liabilities. Utilising the Revised Entrepreneur Relief on CGT is a crucial part of minimising your tax liabilities.

Tips for Maximising Your Use of Revised Entrepreneur Relief

The most important tip is to start planning now. You don’t want to discover at the time of exit that you fail to meet the criteria, especially when changes could have been made to ensure you do qualify. Failing to meet the criteria can mean you can’t maximise your use of the Revised Entrepreneur Relief, or you might not be able to use it at all.

Key parts of advance planning in relation to Revised Entrepreneur Relief include reviewing the following:

- The shareholding structure and/or group structure of your company/holding company should ensure your ownership percentage meets the minimum threshold.

- The period of time the company has been undertaking its qualifying business.

- The trading status of subsidiaries if you have a holding company, as non-trading companies and subsidiaries, could impact whether you qualify.

- Your involvement with the company, i.e., are you involved enough and in the right role to qualify under the criteria for Revised Entrepreneur Relief?

- Assets that do not qualify under the criteria to ensure your calculations are accurate.

- Your records to ensure there is evidence to support your claim for Revised Entrepreneur Relief.

At the time of exit, there are additional considerations, as it’s important the structure of the transaction (such as the sale of your business) keeps you within the criteria of Revised Entrepreneur Relief.

Expert Advice on Revised Entrepreneur Relief and Exit Strategy Planning

As well as providing expert advice on minimising your tax liabilities using Revised Entrepreneur Relief and other levers, we can also help with exit strategy planning. Get in touch today to arrange a consultation.

Latest Blog

Check out our blog and you will get the latest news, events, and financial tips from Gilroy Gannon.

“What's my business actually worth?” This is a question asked…

The fundamentals of statutory audits in Ireland are broadly the…

For some companies in the hospitality sector, as well as…

Agricultural Relief is about facilitating the succession of farm businesses…

Postponed VAT accounting helps Irish businesses improve cash flow by…

Revised Entrepreneur Relief has been around since 2016, but this…

The rate of VAT on the sale of apartments has…

The government’s auto-enrolment pension saving scheme is up and running.…