Property Development in 2026: How the New 9% VAT Rate Impacts Apartment Construction

The rate of VAT on the sale of apartments has been reduced from 13.5% to 9%. This is potentially welcome news for both property developers and buyers.

The main idea behind the reduced VAT rate is to enhance the viability of apartment development projects, especially as costs in the construction sector rise.

The 9% VAT rate is effective from now until the end of 2030. In other words, based on current information, the reduced rate is time-limited. The standard 13.5% rate will continue to apply to most other residential and commercial property transactions.

In this blog, we look at the impact this reduction in VAT will have on apartment construction. We outline the main reasons why the government decided to reduce the rate, the types of developments that will qualify, and what you should do if you are a developer.

Key Motivations for Reducing the VAT Rate on Apartment Transactions in Ireland

Lower the Break-Even Point for Developers

Apartment construction projects often get stuck because the cost of building is higher than apartments can realistically be sold for. There are a number of reasons for this, including higher construction costs. Reducing the VAT rate for apartment transactions helps to make developments more financially feasible.

| Standard VAT Rate of 13.5% | New Rate of 9% until 31 December 2030 | Difference | |

|---|---|---|---|

| Apartment sale price | €350,000 | €350,000 | – |

| VAT amount | €47,250 | €31,500 | €15,750 |

| Total price to buyer | €397,250 | €381,500 | Buyer saves €15,750 |

The Preference for Compact Growth

There is a preference in the National Planning Framework to build new homes within existing city and town footprints. This is easier to achieve with apartment developments than with traditional housing estates.

Build to Sell

The lower 9% rate of VAT on apartment transactions aims to encourage build-to-sell over build-to-rent.

Maintain Construction Momentum

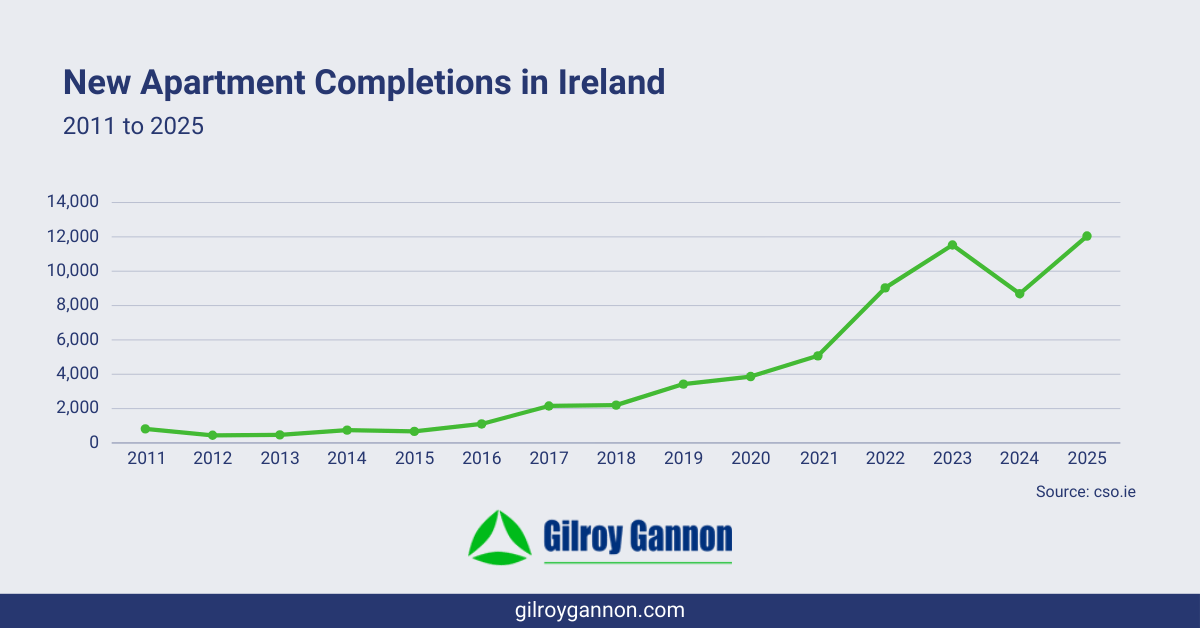

Apartment building has been increasing in recent years, but there are specific reasons for this growth. This includes the temporary waiver on development levies for projects commenced between April 2023 and December 2024, with completion by the end of this year, 2026. The reduction in VAT aims to maintain some of this momentum in apartment development projects.

The Criteria for the Reduced Rate of VAT on Apartment Transactions

There are two key questions when understanding the criteria to qualify for the reduced 9% VAT rate: what is an apartment, and what is an apartment block?

What is an Apartment?

In relation to determining the correct VAT rate, an apartment is a residential unit that is self-contained and located in a building that qualifies as an apartment block. What can be defined as a residential unit is not spelled out, but includes common configurations that people can live in – studio apartments, duplex apartments, penthouse apartments, and student accommodation.

What is an Apartment Block?

The Revenue’s requirements for a building to be categorised as an apartment block include:

- Multi-storey residential building (can be standalone or part of a building).

- Contains no less than three apartments (so excludes small developments).

- Features grouped or common access.

- Each apartment must be structurally contained within the building.

Where the Reduced VAT Rate Won’t Apply

Examples of where the 9% VAT rate won’t apply include:

- An apartment that is the only apartment in a building, such as an apartment in a converted house.

- A building with two apartments.

- Parts of a building located in an apartment block but are not apartments, e.g., commercial units within an apartment block

Grey Areas and Complexities

As with many parts of tax law, there are complexities and grey areas with the reduced VAT rate of 9% on apartment transactions. Examples include

- Mix-use developments – mix-use developments (commercial and residential, for example), where there are shared common areas.

- Own access apartments – apartments with their own access in an apartment block that also has common access are likely to qualify for the 9% VAT rate, but this is another grey area.

- Amenities – amenities in an apartment block, such as a gym or pool, are unlikely to qualify for the 9% VAT rate.

- Cut-off point – the 9% VAT rate only applies up to the point where the apartment can be lived in. Understanding where this point is can be crucial.

- Site and build contracts – site and build contracts can qualify, providing the apartment block criteria are met.

One other area that has caused some confusion is the inclusion in the legislation that the reduction in the VAT rate is “part of a social policy”. This phrase is about the government complying with EU rules on VAT rates rather than a requirement for social housing. In other words, there is no requirement to include a social housing element in an apartment block development to qualify for the lower rate of VAT.

What Should You Do If You Are a Developer?

- Get professional advice to check if the 9% rate of VAT applies.

- Check your contracts to ensure the wording is in line with the Revenue’s definitions, especially in relation to site and build contracts.

- If the apartment block is mixed-use or has amenities, you will probably need to apply different VAT rates for the different parts, i.e., 9% for the apartments and 13.5% for other elements. Again, getting professional advice is the best approach.

- In terms of getting advice, make sure you act early, as the difference between a 9% and 13.5% VAT rate can have a significant impact on profit margins and financial forecasting.

Support at Gilroy Gannon

Among other benefits, the new (albeit temporary) 9% VAT rate on apartment transactions can change the equation, making developments more financially viable. There are potential pitfalls, however.

If you are a property developer and need advice on the new 9% VAT rate on apartments (or any other tax question), contact us at Gilroy Gannon.

Latest Blog

Check out our blog and you will get the latest news, events, and financial tips from Gilroy Gannon.

The fundamentals of statutory audits in Ireland are broadly the…

For some companies in the hospitality sector, as well as…

Agricultural Relief is about facilitating the succession of farm businesses…

Postponed VAT accounting helps Irish businesses improve cash flow by…

Revised Entrepreneur Relief has been around since 2016, but this…

The rate of VAT on the sale of apartments has…

The government’s auto-enrolment pension saving scheme is up and running.…

From 1 January 2026, the national minimum wage in Ireland…